Headquartered in Jakarta and established in 1992, PT Samuel Sekuritas Indonesia (‘SSI’) is a leading local financial institution.

SSI provides a broad range of financial services across investment banking, securities and investment management to a diversified client base including corporations, financial institutions, governments and individuals.

With a track record of success anchored on a strong, dedicated team of highly experienced investment professionals, SSI continues to deliver innovative client financial solutions in Brokerage Services, Research, Corporate Finance and Advisory as well as Fixed Income Sales and Trading.

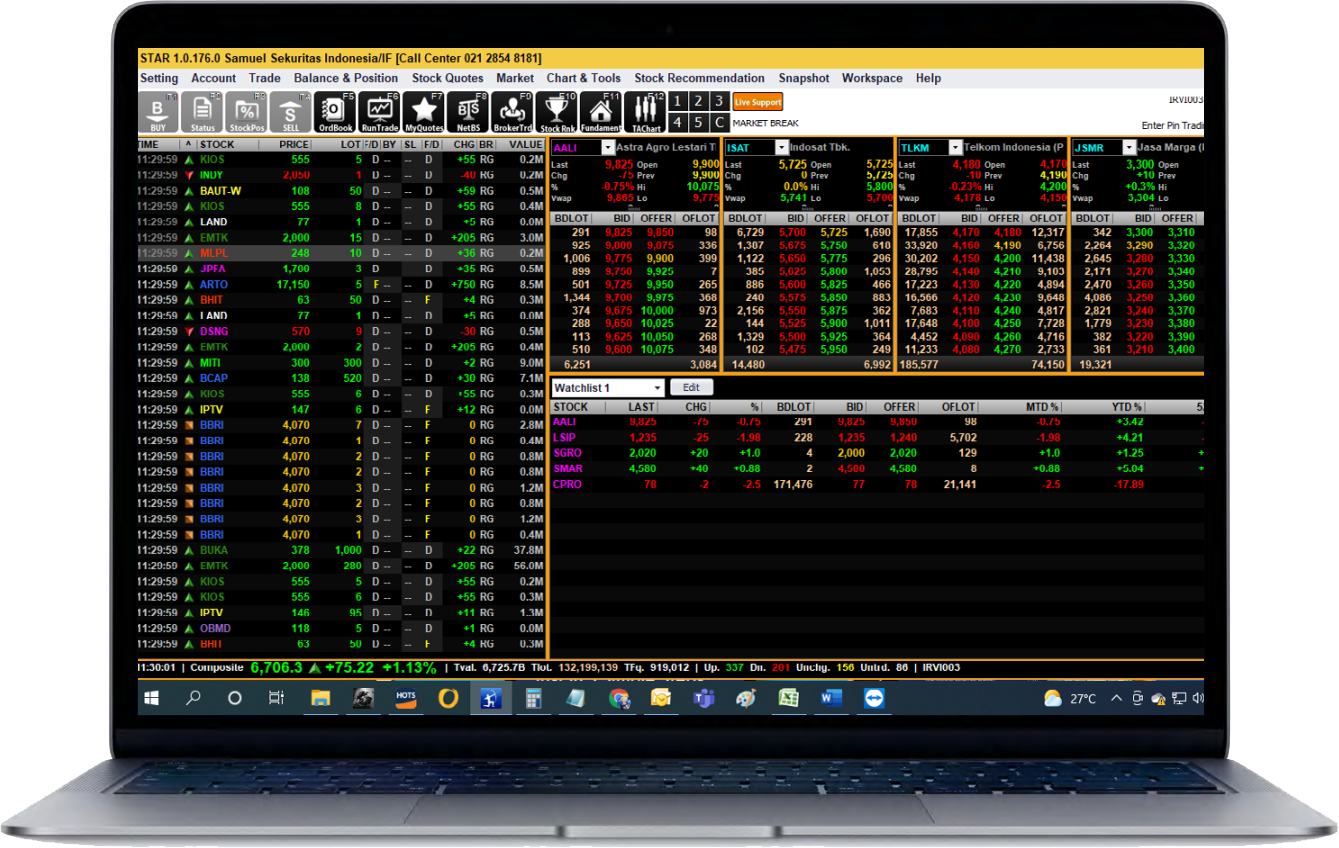

Samuel Trading Active Realtime (‘STAR’) is a leading online trading platform that allows our clients to take advantage of opportunities in today's increasingly complex and dynamic capital markets.

SSIs research provides economic, fundamental analysis as well as timely short-term tactical trading opportunities to create effective investment opportunities and strategies.